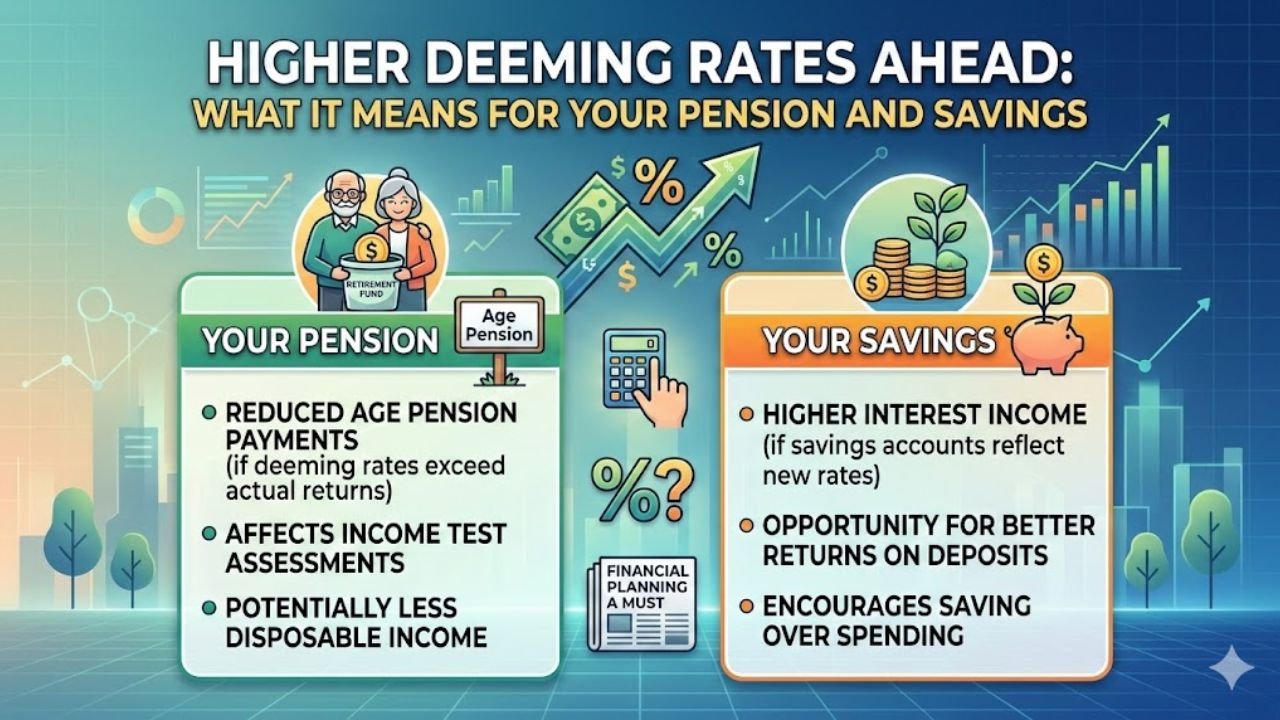

The landscape for Australian retirees is shifting as the federal government moves to normalize social security settings. For several years, pensioners enjoyed a reprieve through a “deeming rate freeze” designed to provide financial stability during the economic volatility of the pandemic. However, with that freeze now a thing of the past, a new era of higher deeming rates has arrived. These changes, effective from 20 March 2026, represent a strategic adjustment to align government assumptions with the actual returns available in the current high-interest market. Understanding how these “invisible” earnings affect your bank account is essential for anyone navigating the Age Pension system.

Understanding the Deeming Mechanism

Deeming is the method Services Australia uses to estimate the income you earn from your financial assets. Rather than requiring you to report every cent of interest or dividend earned, the government assumes your investments earn a set percentage. This “deemed” income is then used to determine your eligibility and payment amount under the pension income test. While this simplifies paperwork, it creates a unique challenge: if the deeming rate rises, the government assumes you are wealthier than before, even if your actual bank balance hasn’t changed. The goal is to ensure the social security system remains fair, but for those on the cusp of income thresholds, even a small percentage hike can lead to a reduction in fortnightly payments.

The March 2026 Rate Hikes Explained

Following the expiration of the long-term freeze, the government has moved toward a “gradual reset” of these rates. Starting 20 March 2026, the lower and upper deeming rates will both see an increase of 0.5 percentage points. This shift is guided by the Australian Government Actuary, marking a transition toward more transparent, data-driven adjustments. While the rates remain below the peak interest rates seen in some term deposits, they are moving closer to the market reality. The specific changes are designed to reflect that retirees can now find better returns on their savings than they could three years ago.

The Impact on Your Fortnightly Pension

The most pressing question for most retirees is how this affects their “take-home” pay. For many, the sting of higher deeming rates will be softened by the concurrent indexation of the Age Pension. Every March and September, pension rates are adjusted to keep pace with inflation. In 2026, the increase in the base pension rate (estimated at $22.20 per fortnight for singles) is expected to largely offset the losses incurred by the higher deeming rates. However, those with significant financial assets—particularly part-pensioners—may find that the higher “deemed income” cancels out a portion of their indexation boost, leaving them with a smaller net increase than their peers.

Savings and Investment Strategy Shift

Higher deeming rates change the math for personal savings. In the past, when rates were frozen at 0.25%, any interest earned above that was “free” and didn’t count against your pension. Now that the upper rate is hitting 3.25%, the “buffer” is shrinking. To maintain your standard of living, it is becoming increasingly important to ensure your money is actually working as hard as the government assumes it is. If your savings are sitting in a legacy account earning 1% while the government deems them to be earning 3.25%, you are effectively being penalized. This shift encourages retirees to shop around for high-interest savings accounts or term deposits that outperform the deeming benchmarks.

Who is Most at Risk?

Not everyone will feel the change equally. Full-rate pensioners with minimal financial assets will likely see no negative impact and will simply enjoy the full benefit of the March indexation. The group most affected consists of “part-pensioners” who are tested under the income test rather than the assets test. Additionally, individuals holding a Commonwealth Seniors Health Card (CSHC) should be cautious; because the CSHC is subject to an income test that includes deemed income, a rise in rates could theoretically push some self-funded retirees over the eligibility limit, causing them to lose access to cheaper medicines and concessions.

Looking Toward the Future

The move to involve the Australian Government Actuary suggests that the era of “set and forget” deeming rates is over. We are entering a period where these rates will likely fluctuate more frequently in response to the Reserve Bank of Australia’s cash rate decisions. For retirees, this means financial planning must become more dynamic. Staying informed about the 20 March and 20 September adjustment dates is no longer optional—it is a core part of managing a retirement budget. By understanding these shifts early, you can adjust your investment allocations to ensure your actual income stays ahead of the government’s assumptions.

FAQs

Q1. Will my pension definitely go down on March 20?

Not necessarily. While higher deeming rates increase your “assessed income,” the general Age Pension rates are also increasing due to indexation. Most people will see a net increase in their bank account, though it may be smaller than expected.

Q2. Does deeming apply to my family home?

No. The family home is an exempt asset and is not subject to deeming. Deeming only applies to financial assets like bank accounts, shares, managed funds, and some superannuation streams.

Q3. What if my actual investments earn less than the deeming rate? Unfortunately, the government uses the deemed rate regardless of your actual earnings. If your bank account pays 0.5% interest but the deeming rate is 1.25%, you are still assessed at the higher 1.25% rate.